Global Corporate Survey 2020: EHS Service Providers Brands Recognition

This report helps strategy executives, chief marketing officers and business development directors at EHS service providers understand the strength of their brand awareness and brand preference in the eyes of 301 customers across 31 countries and 25 industries. Of the 301 senior EHS executives Verdantix interviewed, 74% represented firms with revenues greater than $1 billion and 71% held role titles at the level of director or above. Verdantix research identifies a brand presence gap between large multinational consulting firms and specialized EHS service providers. Firms such as DuPont Sustainable Solutions, which had the highest brand awareness of the 22 service providers considered, benefited from a superior brand perception in the growing Asia Pacific and Latin America EHS services markets.

CORPORATE PERCEPTION OF EHS SERVICE PROVIDERS

This report helps strategy executives, chief marketing officers and business development directors at EHS service providers understand the strength of their brand awareness and brand preference in the eyes of 301 customers across 31 countries. Verdantix conducted the brand assessment study between August and October 2020 via interviews with senior EHS decision-makers who have direct responsibility for corporate-wide EHS management strategies and initiatives.

EHS Service Provider Study Includes Over 300 Executives Across Industries

Which EHS service providers enjoy the strongest brand preference and awareness among senior EHS decision-makers? To find out, Verdantix surveyed EHS decision-makers for their perspectives on the capabilities of 22 EHS service providers’ brands. The 2020 version of the Verdantix survey targeted:

301 representatives of firms with revenues of at least $250 million.

Of the 301 EHS decision-makers interviewed, 74% belonged to firms with revenues of at least $1 billion. The respondents’ demographics included: 27% from firms in the mid-market segment, with revenues of $250 million to $1 billion; 47% from firms in the core enterprise segment, with revenues of $1 billion to $10 billion; and 26% from the large enterprise segment, with revenues above $10 billion. Breaking down the large enterprise segment further, 15% of firms had revenues greater than $20 billion. Among the job titles of the 301 respondents, 35% were in SVP, VP or head of function roles; 36% were in senior director or director roles; and the remaining 29% were in senior manager or manager roles.

25 industries, two-fifths of which have high or very high EHS risk.

The 2020 global survey covered 25 industries, segmented into four categories based on perceived EHS risk: very high, high, medium and low. In aggregate, 39% of the interviewed EHS decision-makers represented industries with high to very high EHS risk profiles. Industries with a very high EHS risk profile – chemicals, mining and metals, and oil and gas – accounted for 16% of respondents. This year’s survey placed the greatest focus on industries with medium EHS risk profiles, totalling 43% of respondents. Industries categorized as medium EHS risk include consumer goods, industrial equipment, and road vehicle manufacturing.

31 countries, focusing on regions with higher levels of EHS spend.

The 301 respondents who participated in the 2020 survey were spread across 31 countries and grouped into five geographical regions: Asia Pacific, Europe, Gulf States and Africa, Latin America and North America. The regions with higher levels of EHS spend – North America and Europe – constituted a larger percentage of the surveyed EHS decision-makers. The North America region – the United States and Canada – made up 28% of respondents, while Europe aggregately accounted for 29%. The Asia Pacific region, which includes China, Taiwan, Vietnam, Thailand, Indonesia, Malaysia, Singapore, India, Australia and New Zealand, accounted for 22% of survey respondents.

CORPORATE BRAND PERCEPTION DATA HIGHLIGHTS A BRAND AWARENESS DIVIDE

Verdantix gathered data from respondents located across 31 countries to provide a comprehensive overview of the perception of EHS service providers among EHS decision-makers. Respondent survey data facilitate insights into brand strength, capabilities, and brand awareness. Throughout the report and figures, percentages are rounded to zero decimal places; the sum of the numbers in a chart may not add to 100%, due to rounding. Verdantix found that:

Asia Pacific footprint boots DSS’s global recognition.

DuPont Sustainable Solutions (DSS), which separated from DuPont in 2019, topped the brand preference rankings, with four-fifths (79%) of respondents rating it as either market-leading or strong in its capabilities as an EHS service provider (see Figure 1). Contributing to DSS’s enhanced brand perception is its significant presence in the Asia Pacific (APAC) region (14 locations across Australia, China, Singapore, Japan, Indonesia, Thailand, South Korea and the Philippines), where half of respondents considered its services to be market-leading. DSS also has an expanding range of services, such as SafetyTech.ai, a recently developed digital platform that enables the deployment of innovative safety technologies.

Global consulting firms benefit from their established brand and wealth of resources.

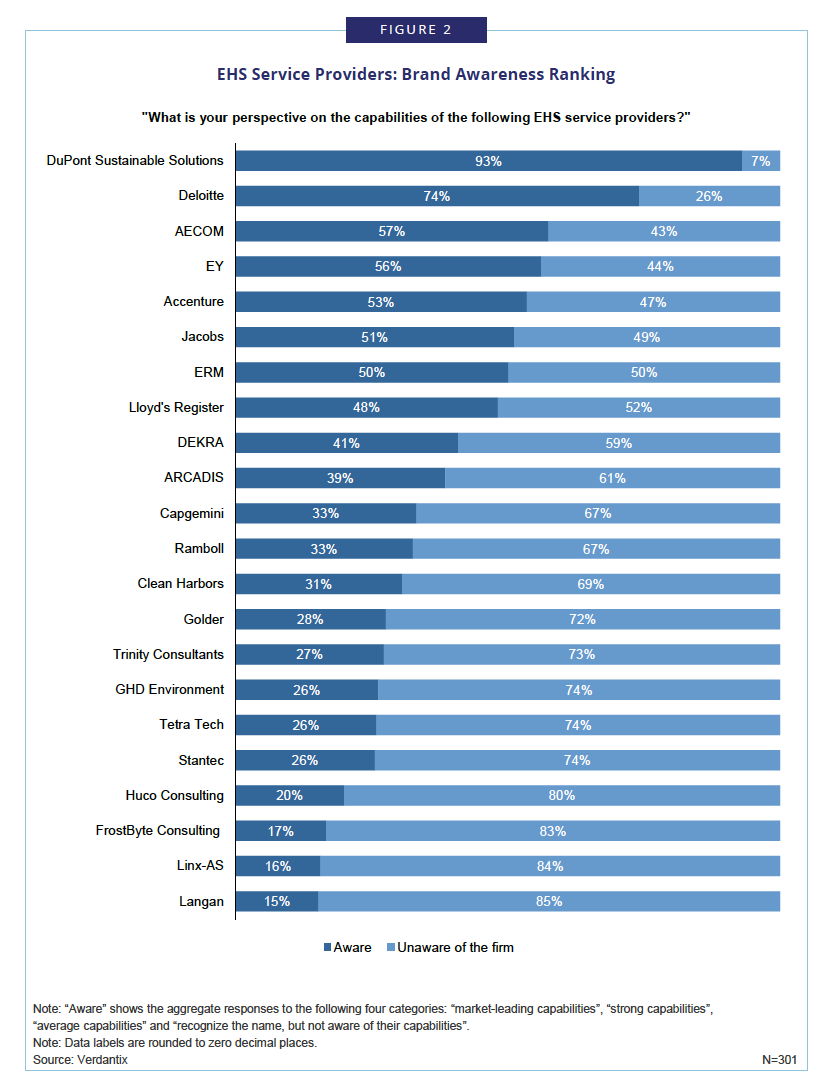

A clear distinction emerged between the perceived EHS service capabilities of large multinational consulting firms and traditional EHS service providers. Professional services firms Accenture, Deloitte and EY, and infrastructure and engineering consultancy firms AECOM and Jacobs, round out the top six service providers when ranked by brand awareness (see Figure 2). Despite EHS forming a small part of their total capabilities, 10% or more of respondents considered Accenture and Deloitte to be market-leading EHS service providers. Both firms benefited from an extremely positive brand perception in the APAC region, reflecting recent strategic investments made there. For example, in 2018 Deloitte announced an additional $321 million investment in the APAC market to be made over three years. Deloitte made this investment decision following analysis that identified APAC as the fastest growing region in its network.

Traditional EHS service providers compete for brand recognition.

Specialist firms exhibited low levels of awareness among the 301 EHS decision-makers interviewed. Brand awareness for the seven firms that traditionally specialize in EHS topics ranged from 16% (Linx-AS) to 31% (Clean Harbors), with all lower than the 39% average. On closer inspection, regional brand presence varied significantly for smaller firms that lack the global reach of companies such as AECOM and Jacobs. Consider Stantec, for example, whose brand awareness among North American-based EHS executives reached 39%, while in Latin America, none of the Brazil or Mexico-based respondents recognized the brand.

SPECIALIST EHS SERVICE PROVIDERS SHOULD AIM TO CLOSE THE BRAND AWARENESS GAP

DSS emerges as the preferred services brand among EHS professionals, bolstered by increased investment and a large presence in the APAC region. Survey data also highlight the gulf in awareness between large consulting firms and specialist EHS service providers. To improve their market presence and reputation, traditional EHS service firms should:

Expand digital capabilities through acquisitions.

The 2020 survey data show that 73% of the 301 surveyed EHS decision-makers consider a consulting provider’s ability to support digitization efforts to be important or very important in influencing vendor decisions. Leading EHS service firms have recognized the need for comprehensive digital implementation capabilities to extend the strength of their offering. Witness Trinity Consultants, which has acquired three EHS technology providers over the last 18 months, increasing its capabilities in process safety management, green buildings and compliance management (see Verdantix Green Quadrant: Digital EHS Services 2020). Trinity Consultants’ recent expansion coincides with a growing global presence and a rise in brand awareness from 21% to 27% over the past year.

View fullsize

Enter the high growth Asia Pacific and Latin America regions.

Recent survey data identify APAC and Latin America as the regions presenting the greatest growth opportunities for EHS service firms. When asked about spend on EHS consulting projects in 2021, respondents located in these areas projected above-average budget increases, with a particular focus on environmental compliance, software implementation and improving operational performance projects (see Verdantix Global Corporate Survey 2020: EHS Budgets, Priorities & Tech Preferences Data Tables). An example of a firm capitalizing on this growth opportunity is ERM, which in 2019 expanded its footprint in Asia by opening a South Korea-based regional operation. The new office location for ReachCentrum, an ERM-owned firm, aims to satisfy growing customer demand arising from emerging chemical regulations in APAC countries. Traditional EHS service firms with a low market presence in these regions include Huco Consulting, Langan, Stantec and Tetra Tech.

Consider strategic partnerships with globally recognized brands.

Survey data identify a gap in awareness between specialized EHS service providers and large consultancies such as AECOM, Deloitte and DSS. This presents an opportunity for smaller firms to partner with global EHS service providers on high-profile projects, extending their reach and creating positive brand associations. Consider Chevron’s work with Accenture, utilizing innovative technologies to reduce crane injuries (see Verdantix Chevron Partners With Accenture To Reduce Crane-Related Industrial Accidents Via Proximity Sensors And Analytics). This high-profile project drew attention to the smaller, more specialized firms involved – Redpoint, Symeo and Trimble.

Written by Christopher Sayers with Rodolphe D’Arjuzon – December 2020